Technology

EximAgent vs Apollo vs TradeAtlas: Best for Exporters?

Jun 29, 2026

Technology

Ireland's exports crashed 36.4% in February 2026 as US pharma frontloading reverses. See what the tariff hangover means for global exporters in 2026.

April 28, 2026By Davos Pham5 min readView as Markdown

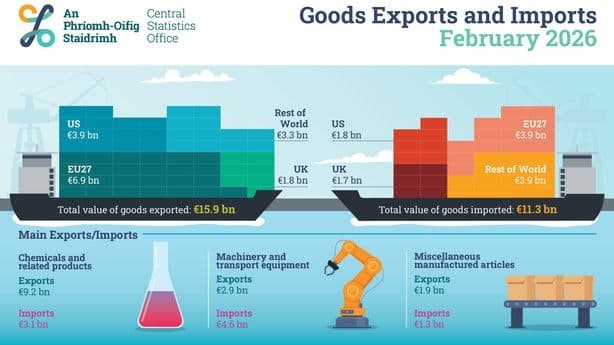

Ireland's goods exports collapsed 36.4% year-on-year to €15.9 billion in February 2026, with US-bound shipments crashing 69.7%. The drop is not a demand crisis — it's the unwinding of 2025's pharmaceutical frontloading rush ahead of US tariffs. Exporters globally should treat this as a leading indicator: tariff-driven distortions are now reversing across multiple trade corridors, and 2026 comparison baselines will remain skewed for months.

Metric | February 2026 | YoY Change |

|---|---|---|

Total exports | €15.9 billion | ▼ 36.4% |

Exports to US | €3.9 billion | ▼ 69.7% |

Total imports | €11.3 billion | ▼ 6.1% |

US share of exports | 24.7% | Down from 51.8% |

Chemicals & pharma exports | €9.2 billion | Still dominant |

Top export partners (Feb 2026): United States (24.7%) → Netherlands (17.7%) → Great Britain (8.7%) Top import partners (Feb 2026): United States (16.1%) → Great Britain (11.7%) → China (8.5%)

In late 2024 and early 2025, exporters across Asia, Europe, and Latin America rushed shipments into the United States ahead of expected tariff hikes. Ireland's pharmaceutical sector was one of the most aggressive frontloaders — and now the reversal is visible in cold numbers.

If you ship to the US from Vietnam, India, Malaysia, or anywhere else, expect similar Y/Y distortions in your own data through Q2 and Q3 2026. Your sales team's "decline" may not be a real decline.

Both Ebury and Deloitte Ireland flagged the same point in the CSO release: compared to 2024 (a normal year), Ireland's exports are essentially stable. The 36.4% headline only exists because 2025 was abnormal.

Translation for exporters: Stop benchmarking 2026 against 2025. Use 2024 or a 24-month rolling average until tariff distortions clear.

Cost pressures are stacking on top of the tariff unwind:

After working with hundreds of SME exporters across Vietnam, India, Malaysia, and the US through the EximAgent platform, here's what the Ireland data actually tells us:

Deloitte's Louise Kelly captured the most important framing: "This is a reset after an exceptional year, with the real signal now emerging beneath the headline numbers."

For trade professionals, three things to monitor through Q2–Q3 2026:

EximAgent and EximAgent are AI-powered trade intelligence tools built for exactly this kind of market — where headline numbers mislead and the real signal sits inside HS codes, buyer concentration, and FTA coverage.

The exporters who win in 2026 won't be the ones with the biggest 2025 numbers. They'll be the ones who saw the reset coming first.

Source: Ireland Central Statistics Office (CSO), April 2026. Commentary from Robert Purdue (Ebury Ireland) and Louise Kelly (Deloitte Ireland).

Enter your email to receive the latest trade insights, guides, and HS-code explainers from EximAgent Blog.